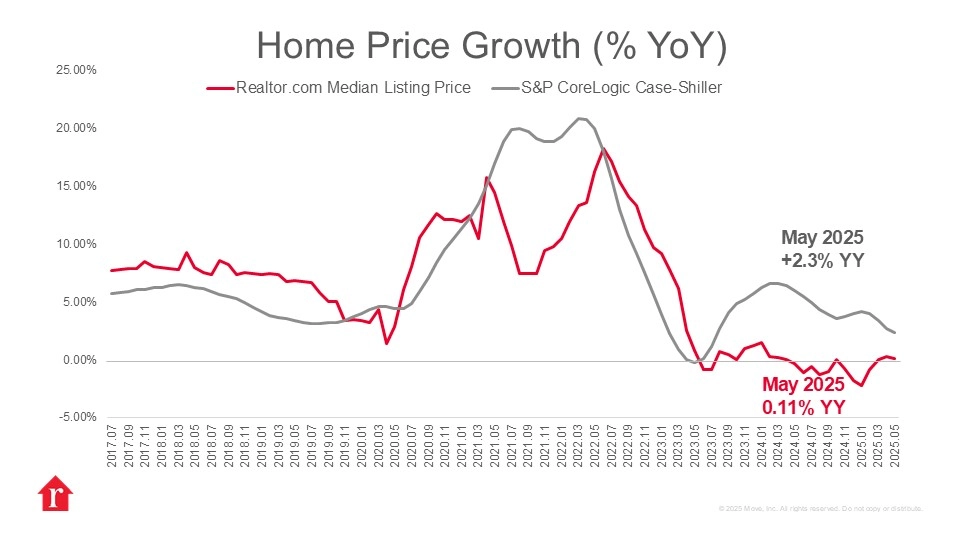

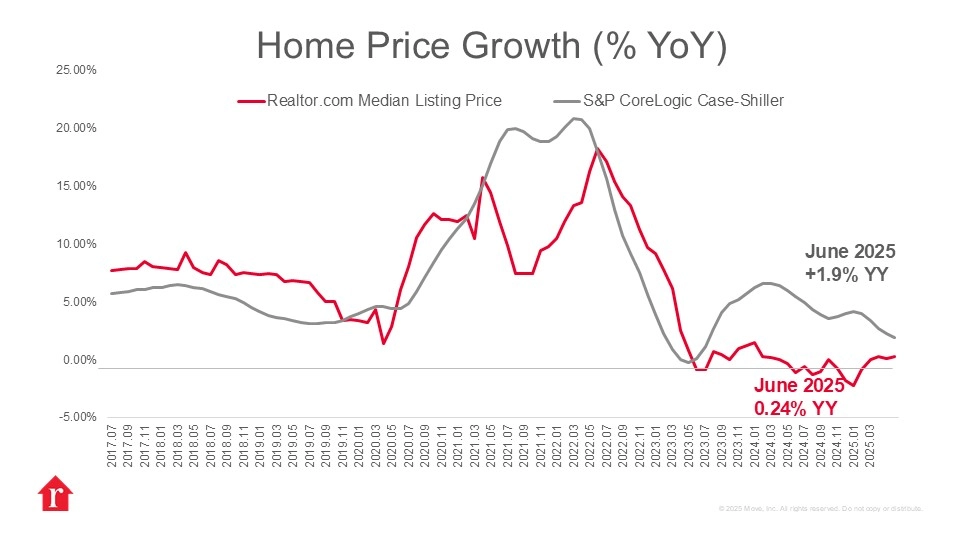

The S&P CoreLogic Case-Shiller Index showed a further slowdown in home price growth in June, with the national index rising 1.9% year over year, down from 2.3% in May, as affordability constraints, elevated supply, and uneven regional demand continue to weigh on housing activity. This months release reflects sales from April through June, a period of stable mortgage rates below 7% , muted buyer sentiment, and growing price sensitivity.

While home prices remain higher than one year ago, the pace of appreciation moderated in June. Realtor.com data shows median list prices rose just 1.2% year over year, down from 2% in May, while months supply ticked up to 4.6, approaching a 10-year high . Inventory gains and longer selling timelines in Sun Belt metros are putting downward pressure on prices, especially in the South and West.

How did trends vary by region?

Regional price trends remain highly dependent on inventory composition. In high-supply markets like Austin and Jacksonville, increased competition from builders offering incentives and price cuts has added pressure to resale values. In contrast, Midwest and Northeast metros remain tighter, with new construction still commanding a premium of over 50% compared to existing homes. The Realtor.com� July Housing Market Trends Report shows active inventory rose 24.8% year over year, while homes spent a median of 58 days on market, 7 days longer than last year, pointing to an ongoing rebalancing process.

What is ahead for housing?

Looking ahead, the Federal Reserves shift in tone at Jackson Hole has raised the odds of a rate cut in September, which could support affordability later this year. But for Junes Case-Shiller data, that impact has yet to arrive. Instead, the report is likely to underscore a housing market that is normalizing, shaped by local supply dynamics, lingering rate pressure, and a still-cautious consumer base.